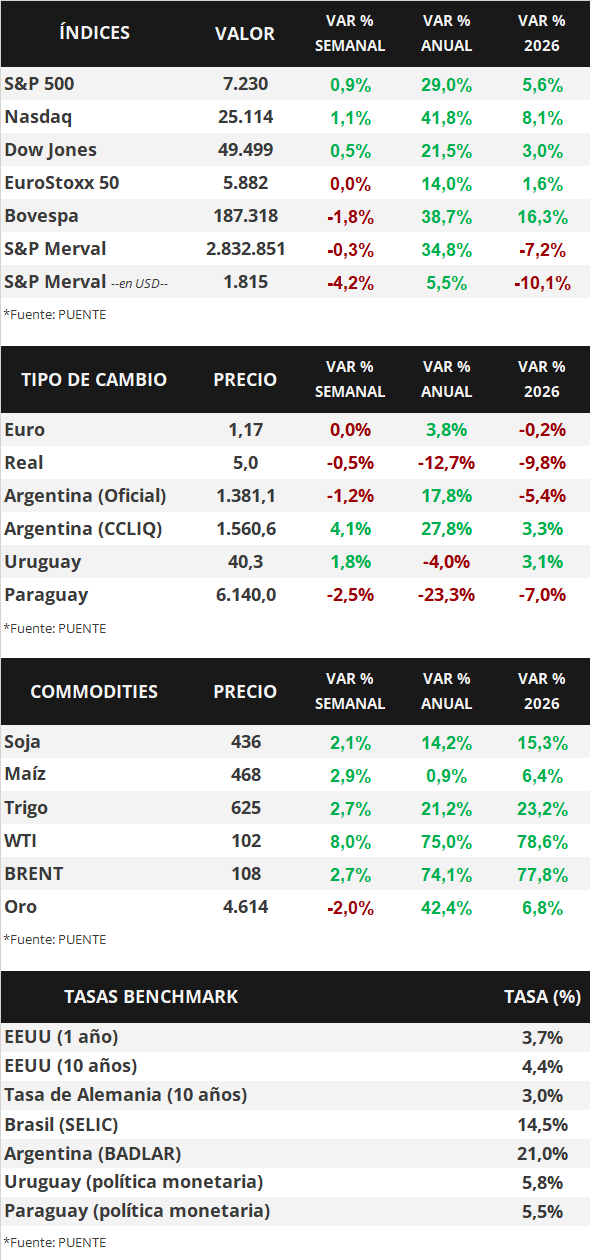

The US Federal Reserve (Fed) held its benchmark interest rate steady in the current range of 3.5%-3.75%, in line with expectations. Meanwhile, the Personal Consumption Expenditures (PCE) price index—the Fed's benchmark for monetary policy decisions—was released for March, showing a 3.2% year-over-year increase in the core (excluding food and fuel) component. The first estimate of first-quarter Gross Domestic Product (GDP) also came in, showing annualized growth of 2.0%, slightly below projections. Five of the "Magnificent Seven" companies reporting first-quarter results exceeded expectations for earnings per share (EPS) and revenue. Against this backdrop, stock indices closed higher, with the S&P 500 and Nasdaq reaching new all-time highs, while the US Treasury yield curve broadened, with the 10-year bond yield at 4.4%. This week, the focus will be on data regarding the evolution of the labor market in April, with the creation of 73 new jobs and an unemployment rate of 4.3%. Meanwhile, expectations remain high for an agreement with Iran. With potential short-term inflationary risks, interest rates are expected to remain historically high, making it advantageous to secure higher nominal returns now compared to those that could be obtained later for investment-grade bonds, with positions in maturities of up to five years being a good option. Separately, the European Central Bank also kept its benchmark interest rate unchanged at 2.15% per annum.

Weekly Monitor

International

This week's focus in the United States will be on the release of the April labor market report, with an estimated 73,000 new jobs created and an unemployment rate of 4.3%. Additionally, the March trade balance will be released, while the first-quarter earnings season continues and the world awaits an agreement with Iran to end the conflict in the Middle East. In Latin America, April inflation figures will be released for Brazil, Chile, and Mexico, with the latest figures showing year-over-year increases of 4.1%, 2.8%, and 4.6%, respectively. Mexico will also hold an interest rate decision, with the current rate at 6.75%.

The Fed held the benchmark interest rate unchanged in its current range of 3.50%-3.75%, in line with expectations. This decision, Powell's last under his leadership, was justified based on a labor market with low average job creation and stable unemployment, alongside high inflation, partly due to the global increase in energy prices. The Fed also expressed uncertainty regarding the economic outlook due to the geopolitical conflict, and stated that it will continue to monitor data developments to balance the risks of its dual mandate: price stability and full employment.

Meanwhile, PCE inflation—the Fed's preferred indicator for monetary policy decisions—in March was in line with expectations, registering a monthly increase of 0.7% and an annual increase of 3.5%, while core inflation rose 0.3% monthly and 3.2% annually. It is worth noting that an acceleration was recorded in almost all measures. On the other hand, first-quarter GDP grew at an annualized rate of 2.0%, according to the initial estimate, lower than the 2.2% forecast by analysts, but better than the performance of the previous quarter.

Regarding the first-quarter earnings season, Alphabet, Microsoft, Amazon, Meta Platforms, Apple, Coca-Cola, Visa, T-Mobile US, Starbucks, General Motors, Kimberly-Clark, AbbVie, Caterpillar, Mastercard, Eli Lilly, and Colgate-Palmolive reported earnings per share (EPS) and revenue above expectations. Verizon, however, only exceeded its EPS projection but not its revenue projection, while Novartis and Barclays reported lower-than-expected EPS and revenue. This week, Pfizer, McDonald's, Mercado Libre, Airbnb, HSBC, Walt Disney, Palantir, and CVS Health, among other major companies, will report their results.

Against this backdrop, the US Treasury yield curve broadly widened during the week. Thus, the 1-year bond yield rose from 3.66% to 3.71%, the 3-year bond yield from 3.80% to 3.89%, and the 10-year bond yield from 4.30% to 4.38%. Meanwhile, investment-grade corporate bonds (LQD ETFs) closed with a yield of 5.6%. Elsewhere, the main US stock indices traded higher, with the Nasdaq and the S&P 500 reaching new all-time highs for the week.

The European Central Bank kept its monetary policy rate unchanged at 2.15% for the seventh consecutive session. ECB President Maria Lagarde noted that upside risks to inflation have intensified and growth has slowed, leading the Committee to discuss a possible increase in the cost of financing at its next meeting in June. Earlier, April's inflation figures were released, showing a 3.0% year-on-year increase and a 2.2% rise in core inflation, in line with expectations. Meanwhile, first-quarter GDP showed a slowdown, growing 0.8% year-on-year and 0.1% quarter-on-quarter, below projections. Against this backdrop, the euro gained 0.4% weekly to $1.17 per euro, while the yield on the 10-year German Treasury bond rose to 3.04%.

Monetary policy meetings were also held in England, Japan, Chile, and Brazil. In the first three cases, central banks opted to maintain interest rates at current levels of 3.75%, 0.75%, and 4.5%, respectively, in line with projections. In Brazil, however, the rate was cut by a quarter of a percentage point to 14.5%, contrary to the consensus expectation among analysts that it would remain unchanged.