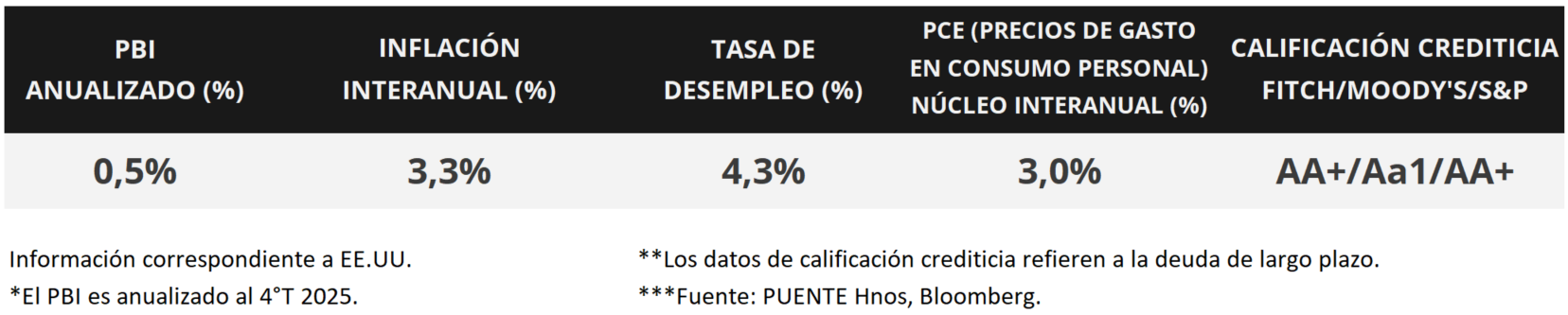

In the United States, March inflation came in below expectations, rising 3.3% year-over-year and 2.6% in the measure that excludes food and energy (core), while the Personal Consumption Expenditures (PCE) price index—the Federal Reserve’s (Fed) preferred measure of inflation for monetary policy decisions—rose by +3.0% year-over-year in February on a core basis, slightly lower than in January. In terms of economic activity, fourth-quarter Gross Domestic Product (GDP) was revised downward, growing at an annualized rate of +0.5% and resulting in a +2.1% annual rate for 2025. In this environment, U.S. Treasury yields closed with mixed results, with the 10-year bond at 4.32%; meanwhile, major stock indices ended the day in positive territory, with the Nasdaq standing out. This week, attention will focus on the start of the first-quarter corporate earnings season, while on the geopolitical front, a final agreement with Iran is expected to be reached. Given that inflationary risks are persistent, interest rates are expected to remain high by historical standards (currently at 3.75%) throughout the year. Consequently, it is advisable to secure higher nominal yields today compared to those that might be available later for investment-grade bonds, with a favorable strategy being to position oneself in maturities of up to 5 years.

Weekly Monitor

International

The focus this week in the United States will be on the start of the Q1 2026 corporate earnings season, with the financial sector releasing its financial results. Meanwhile, attention will remain on the unfolding geopolitical conflict in the Middle East, as markets await a final agreement; on the data front, March’s producer price inflation figures will be released. In the Eurozone, the final estimate of the March consumer price index will be released, with an annual increase of +2.5% projected and +2.3% for the core measure. Finally, in China, first-quarter GDP will be released, with an estimated +4.8% year-over-year growth.

In the United States, March inflation came in below expectations across all measures, registering a +0.9% monthly increase and a +3.3% year-over-year rise, accelerating significantly from February due to the impact of energy prices; meanwhile, the measure excluding food and energy (core) rose +0.2% monthly and +2.6% annually.

Meanwhile, February’s PCE inflation—the Fed’s preferred indicator for monetary policy decisions—came in line with expectations, posting a year-over-year increase of +2.8% and +3.0% for the core measure, the latter figure slightly lower than in January. On a month-over-month basis, it rose +0.4% across both measures. On the other hand, fourth-quarter 2025 GDP grew by +0.5% on an annualized basis, according to the final estimate, versus the expected +0.7%. Thus, 2025 closed with an annual expansion of +2.1%, below previous years.

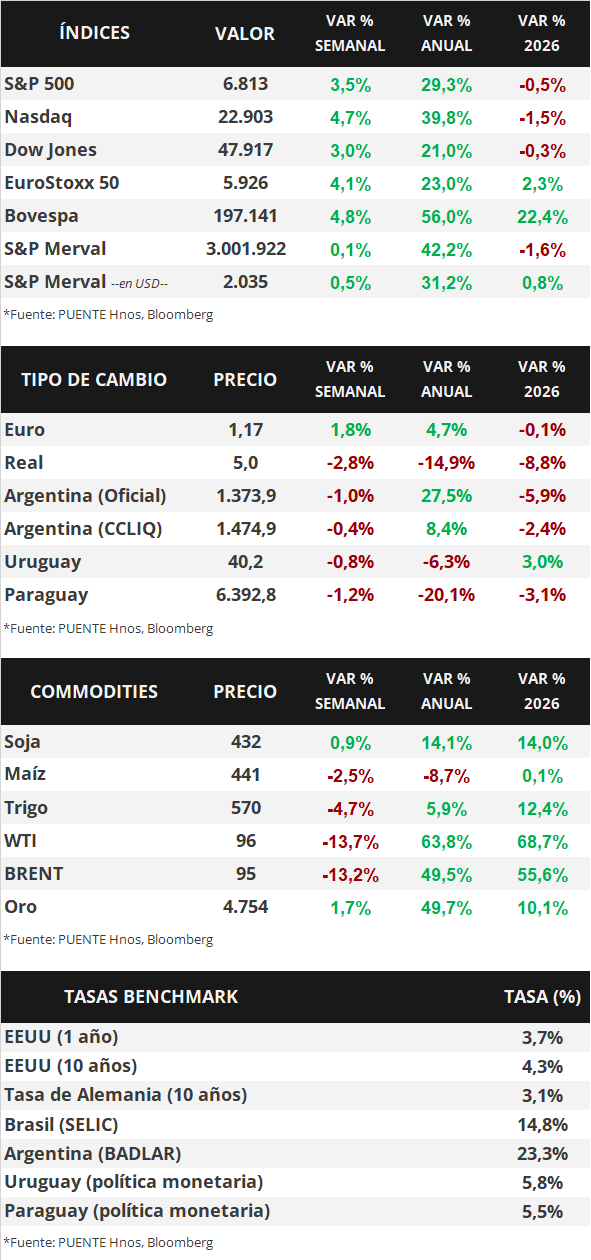

In this environment, U.S. Treasury bond yields traded mixed during the week. The 1-year bond rose from 3.65% to 3.68%, the 3-year bond remained at 3.82%, and the 10-year bond rose from 4.30% to 4.32%. Meanwhile, investment-grade corporate bonds (LQD ETF) closed with a yield of 5.5%. On the other hand, the major U.S. stock indices extended their upward trend, with the Nasdaq performing best, up 4.7% for the week.

On the geopolitical front, over the weekend, President Trump announced that the U.S. Navy will implement a naval blockade of the Strait of Hormuz, intercepting all maritime traffic entering and leaving Iranian ports and coastal areas. The measure will take effect starting this morning, in response to last week’s failed negotiations and Tehran’s intention to charge a toll for passage through the Strait of Hormuz.

As the 2026 first-quarter corporate earnings season kicks off, major companies reporting this week include Goldman Sachs, JP Morgan, Wells Fargo, Citigroup, BlackRock, Bank of America, Morgan Stanley, Bank of New York Mellon, Progressive, Taiwan Semiconductor, Netflix, PepsiCo, and Johnson & Johnson.

In Latin America, the March consumer price index was also released in Brazil, Mexico, and Chile. In Brazil, the index rose by 4.1%, exceeding expectations; in Mexico, it rose by 4.6% year-over-year, in line with forecasts; and in Chile, it rose by 2.8% year-over-year, surpassing expectations. It is worth noting that in all cases, the rate of increase accelerated compared to February, due to the impact of the war in the Middle East and its implications for energy costs.