In the United States, the Personal Consumption Expenditures (PCE) price index—the Federal Reserve's (Fed) benchmark for monetary policy decisions—rose to an annualized rate of 4.1% in May, and the core PCE index, excluding food and energy, increased by 3.4%, accelerating from the previous quarter. Meanwhile, first-quarter GDP grew at an annualized rate of 2.1%, exceeding analysts' consensus expectations and the performance of the previous quarter. Against this backdrop, the US Treasury yield curve compressed across the board, with the 1-year Treasury yield at 3.91% and the 10-year yield at 4.37%. June's labor market data will be released this week, with an estimated 115,000 new jobs created and unemployment remaining stable at 4.3%. In a scenario of higher short-term inflationary risks and a stable labor market, it is expected that the benchmark interest rate (currently at 3.75%) will remain at historically high levels, allowing for higher nominal returns for longer periods for investment-grade bonds, with the 5-year maturity segments of the yield curve looking attractive.

Weekly Monitor

International

This week's focus in the United States will be on the labor market data for June, with expectations of 115,000 new jobs created and an unemployment rate of 4.3%. In the Eurozone, the preliminary June inflation estimate will be released, projecting a year-on-year increase of 3.1% and a core inflation rate of 2.6%.

In the United States, the PCE inflation rate—the Fed's preferred measure of inflation for interest rate decisions—for May was in line with projections, rising 0.4% month-on-month and 4.1% year-on-year, while the core inflation rate rose 0.3% month-on-month and 3.4% year-on-year. It is worth noting that the year-on-year figures accelerated compared to the previous month.

In terms of economic activity, the final estimate of Q1 GDP showed annualized growth of 2.1%, above the previously recorded 1.6% and the consensus forecast. This performance, even better than that of the previous quarter, reflects economic resilience in a context of uncertainty due to the conflict in the Middle East.

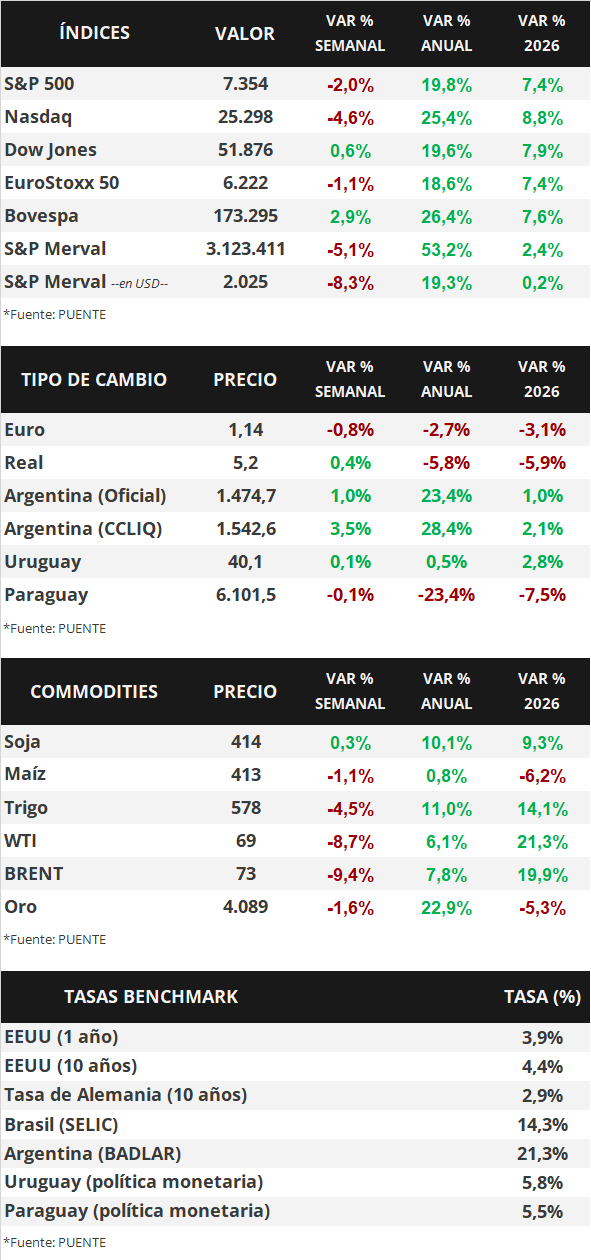

In this environment, US Treasury yields compressed across the entire curve during the week. The 1-year Treasury yield fell from 3.97% to 3.91%, the 3-year yield from 4.19% to 4.09%, and the 10-year yield from 4.45% to 4.37%. Meanwhile, investment-grade bonds (LQD ETFs) finished with a yield of 5.5%. For their part, the main US stock indices had mixed performances, with the Dow Jones standing out with a weekly increase of 0.6%.

In the Eurozone, preliminary Purchasing Managers' Indices (PMIs) – leading indicators of economic activity – for June showed 51.3 points for manufacturing and 48.9 points for services. It's important to note that a reading above 50 points indicates expansion, while a reading below 50 indicates contraction.

Finally, in Latin America, the Bank of Mexico held its monetary policy meeting, where it decided to keep the interest rate unchanged at 6.5% annually. In this context, the exchange rate ended the week with a gain of 0.9%.