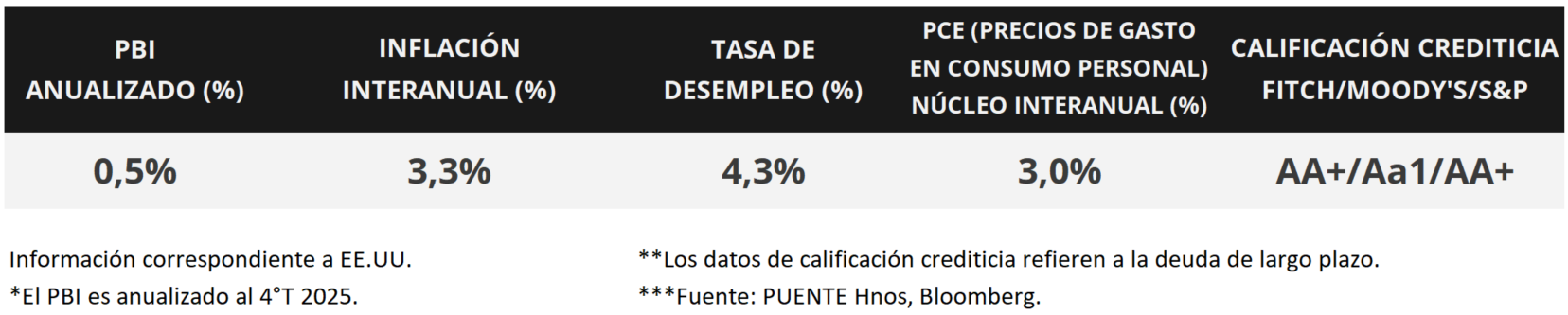

In the United States, wholesale inflation in March rose 4.0% year-over-year, accelerating from the previous reading due to higher energy costs stemming from the war in the Middle East, and 3.8% in the measure excluding food and energy (core). In this environment, the S&P 500 and Nasdaq stock indices ended the week at new all-time highs, while U.S. Treasury yields compressed across the entire curve, with the 1-year bond at 3.63% and the 10-year bond at 4.25%. This week, attention will remain focused on the first-quarter corporate earnings season and the geopolitical front, as hopes grow for a deal with Iran that would end the conflict. This scenario is generating greater short-term inflationary pressures, so interest rates are expected to remain high by historical standards (currently at 3.75%) for the rest of the year. In this regard, it remains advisable to secure higher nominal yields today compared to those that might be available later for investment-grade bonds, with a favorable strategy being to position oneself in maturities of up to 5 years.

Weekly Monitor

International

The focus in the United States this week will remain on the first-quarter 2026 corporate earnings season and the progress of negotiations with the Middle East, as markets await a final agreement. In addition, the University of Michigan’s April Inflation Expectations Survey will be released, with expectations at +4.8% for the next 12 months, along with March retail sales figures. Meanwhile, preliminary April data on the sectoral Purchasing Managers’ Indexes (PMIs) compiled by S&P Global for the United States and the Eurozone will be released.

In the United States, March wholesale inflation came in below estimates in most cases. Specifically, it rose +0.5% month-over-month and +4.0% year-over-year, with the latter accelerating compared to February due to rising energy prices. Meanwhile, the measure excluding food and energy (core) rose +0.1% month-over-month and +3.8% year-over-year, both lower than the previous month.

With the start of the Q1 2026 earnings season, Goldman Sachs, JP Morgan, Citigroup, BlackRock, Johnson & Johnson, Bank of America, Morgan Stanley, Bank of New York Mellon, Taiwan Semiconductor, PepsiCo, and Netflix reported earnings per share (EPS) and revenue above expectations. On the other hand, Wells Fargo only beat the EPS forecast but not revenue, while Progressive had higher-than-expected revenue but lower-than-expected EPS. This week, UnitedHealth, Tesla, Philip Morris, IBM, AT&T, Moody’s, Reckitt Benckiser, Caterpillar, Intel, Nestlé, American Express, Blackstone, Lockheed Martin, and Procter & Gamble, among other major companies, will report earnings.

In this context, the U.S. Treasury yield curve flattened broadly throughout the week. Thus, the 1-year Treasury yield fell from 3.67% to 3.63%, the 3-year yield from 3.82% to 3.72%, and the 10-year yield from 4.32% to 4.25%. Meanwhile, investment-grade corporate bonds (LQD ETF) closed with a yield of 5.5%. On the other hand, the major U.S. stock indices continued to rise, with the S&P 500 and the Nasdaq reaching new all-time highs.

In the Eurozone, the final March consumer price index data was released, showing a monthly increase of +1.3% and an annual increase of +2.6%, exceeding analysts’ consensus forecasts and accelerating from February due to rising energy prices. The measure excluding food and energy (core) rose +0.8% month-over-month and +2.3% year-over-year, in line with expectations. Against this backdrop, the euro gained +0.4% for the week to $1.18 per euro, while the yield on the 10-year German government bond fell to 2.96%.

China’s economy expanded by +5.0% year-over-year in the first quarter, exceeding the estimated +4.6%, and by +1.3% quarter-over-quarter. It is worth noting that these results mark an acceleration compared to previous readings, amid multiple global challenges.

Regarding the performance of Latin American sovereign debt, yields on 10-year dollar-denominated bonds in Brazil and Mexico rose from 5.89% and 5.81% at the start of the previous week to their current levels of 5.90% and 5.74%, respectively.

Translated with DeepL.com (free version)