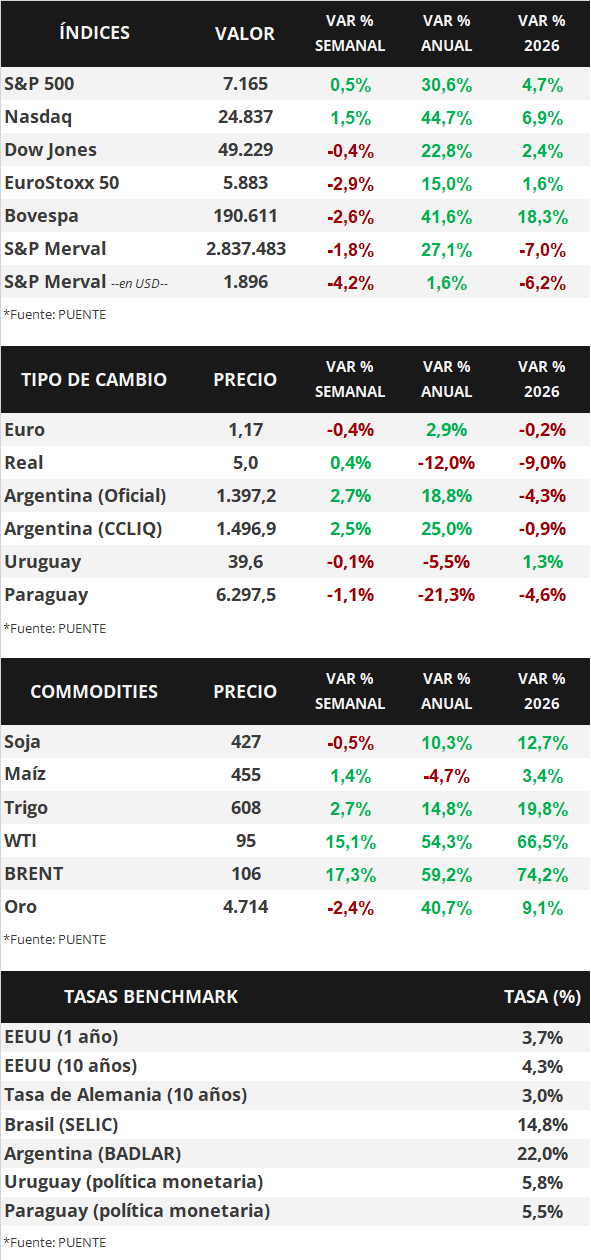

In the United States, the first-quarter corporate earnings season is still underway, with 28% of companies having reported their results. To date, earnings per share are up 15.1% year-over-year, and revenue is up 10.3%, exceeding estimates from late March. In this environment, U.S. Treasury yields widened across the entire curve, with the 1-year note at 3.66% and the 10-year note at 4.30%, while the S&P 500 and Nasdaq stock indices reached new all-time highs. This week, the focus will be on the Federal Reserve’s (Fed) decision, with expectations that it will keep the benchmark rate in the current range of 3.5%–3.75%. In addition, the March Personal Consumption Expenditures (PCE) price index—the Fed’s inflation benchmark for monetary policy decisions—will be released, with a projected annual increase of +3.2% in the measure excluding food and energy, and the first estimate of first-quarter Gross Domestic Product (GDP), with an annualized growth rate of +2.2% projected. Regarding the first-quarter earnings season, reports are expected from 5 of the “Magnificent Seven.” Given potential short-term inflationary risks, interest rates are expected to remain high by historical standards, so it seems prudent to secure higher nominal yields today compared to what might be available later for investment-grade bonds, with a focus on positions with maturities of up to 5 years.

Monitor Semanal

Internacional

The focus this week in the United States will be on the Federal Reserve’s (Fed) monetary policy meeting, with expectations that it will keep the benchmark rate in the current range of 3.5%–3.75%. Additionally, March PCE inflation—the Fed’s benchmark for interest rate decisions—will be released, with estimates pointing to a year-over-year increase of +3.5% and +3.2% for the measure excluding food and energy (core), along with the first estimate of first-quarter GDP, projected to grow at an annualized rate of +2.2%. Regarding the first-quarter earnings season, five of the “Big Seven” will report. Meanwhile, in the Eurozone, preliminary April inflation and first-quarter GDP will be released, with GDP estimated to have increased by +0.8% year-over-year; while monetary policy decisions are also expected in the Eurozone, the UK, Japan, Brazil, and Chile, with interest rates projected to remain at current levels of 2.15%, 3.75%, 0.75%, 14.75%, and 4.5%, respectively.

Regarding the Q1 2026 corporate earnings season, 28% of companies reported results, of which 84% beat earnings per share (EPS) estimates and 81% beat revenue estimates. During the week, Tesla, UnitedHealth, Philip Morris, IBM, AT&T, Moody’s, Intel, American Express, Blackstone, and Procter & Gamble reported EPS and revenue above expectations. On the other hand, 3M only beat the EPS forecast but not revenue, while Lockheed Martin reported lower-than-expected EPS and revenue. This week, five of the “Magnificent Seven”—Alphabet, Microsoft, Amazon, Meta Platforms, and Apple—will report results, along with Caterpillar, AbbVie, Verizon, Coca-Cola, T-Mobile US, Novartis, Visa, Mastercard, Eli Lilly, Glencore, Starbucks, Barclays, General Motors, Kimberly-Clark, and Colgate-Palmolive, among the major companies.

In the United States, preliminary data for the Purchasing Managers’ Indexes (PMIs)—leading indicators of economic activity—for April, as measured by S&P Global, exceeded expectations across all sectors and surpassed March’s figures. Specifically, the manufacturing PMI stood at 54 points, the services PMI at 51.3, and the composite PMI at 52 points. It is worth noting that a reading above 50 points indicates expansion, while one below 50 points indicates contraction in activity.

Against this backdrop, the U.S. Treasury yield curve widened broadly throughout the week. Thus, the 1-year Treasury yield rose from 3.63% to 3.66%, the 3-year yield from 3.72% to 3.80%, and the 10-year yield from 4.25% to 4.30%. Meanwhile, investment-grade corporate bonds (LQD ETF) closed with a yield of 5.5%. On the other hand, major U.S. stock indices traded mixed, with the Nasdaq and the S&P 500 reaching new all-time highs.

In the Eurozone, preliminary April readings for the sectoral PMIs were also released. The manufacturing PMI registered 52.2 points, above expectations, while the services and composite PMIs stood at 47.4 and 48.6 points, respectively—below expectations and the 50-point threshold indicating expansion of activity.