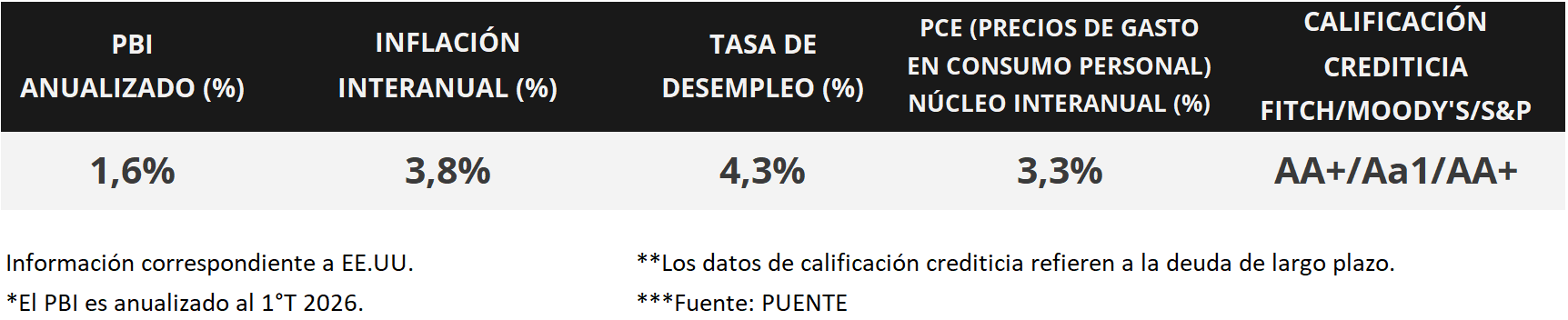

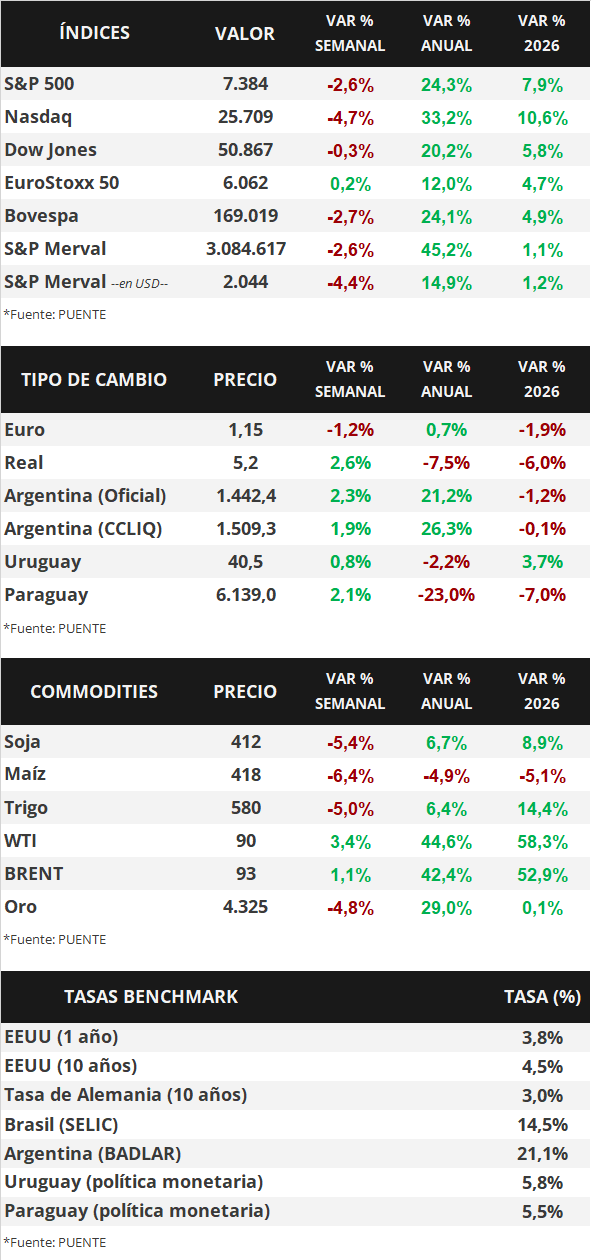

In the United States, the labor market's performance in May once again exceeded analysts' consensus projections, with 172,000 new jobs created compared to the 85,000 expected. April's figure was revised upward to 179,000 jobs. Meanwhile, the unemployment rate remained stable at 4.3% for the third consecutive month. Against this backdrop, US Treasury yields widened across all maturities, with the 1-year bond at 3.84% and the 10-year bond at 4.53%. Stock indices reached new all-time highs across the board during the week. With persistently high inflation expected, exceeding the Federal Reserve's target, the benchmark interest rate (currently at 3.75%) is likely to remain historically high. This scenario allows for higher nominal returns today compared to those that could be obtained later for investment-grade bonds, making it advisable to position oneself in the sections of the curve up to 5 years in duration.

Weekly Monitor

International

This week's focus in the United States will be on the release of the May Consumer Price Index (CPI), with expectations of a year-over-year increase of 4.2% and a 2.9% increase for the core inflation rate (excluding food and energy). Wholesale inflation for the same month and the April trade balance will also be released. Meanwhile, developments are awaited on the geopolitical front regarding the scope of an agreement between the United States and Iran. In Europe, the European Central Bank (ECB) will hold its monetary policy meeting, with an increase to 2.4% expected from the current 2.15%. Finally, in Latin America, May inflation figures will be released for Brazil, Mexico, and Chile, with the latest annual figures being 4.4%, 4.5%, and 4.0%, respectively.

In the United States, 172,000 new jobs were created in May, more than double the consensus forecast of 85,000 and slightly lower than the revised figure of 179,000 for April (down from 115,000). Meanwhile, the unemployment rate remained stable at 4.3% for the third consecutive month, in line with expectations.

Against this backdrop, US Treasury yields broadened across the curve during the week. The 1-year Treasury yield rose from 3.77% to 3.84%, the 3-year yield from 4.05% to 4.20%, and the 10-year yield from 4.43% to 4.53%. Investment-grade bonds (LQD ETFs) finished with a yield of 5.5%. Meanwhile, the main US stock indices all reached new all-time highs, despite ending the week with losses.

In the Eurozone, the preliminary May inflation figure showed a monthly increase of 0.1% and a year-on-year increase of 3.2%, in line with expectations. Core inflation rose 0.3% month-on-month and 2.5% annually, the latter slightly above expectations (2.4%). On the other hand, first-quarter GDP grew 0.3% year-on-year, slowing compared to the previous period and falling short of the 0.8% estimated by analysts. Against this backdrop, the euro weakened 1.2% to $1.15, while the yield on the 10-day German Treasury bond closed at 3.04%.