This week's focus in the United States will be on the release of the PCE inflation figure—the Fed's preferred measure of inflation for monetary policy decisions—for May, with expectations of a 4.1% annual increase and a 3.4% increase in core inflation. The final estimate of first-quarter GDP will also be released, projecting annualized growth of 1.6%. Additionally, preliminary June Purchasing Managers' Indices (PMIs)—leading indicators of economic activity—will be published for the United States and the Eurozone. Finally, in Latin America, Mexico will hold another monetary policy meeting, with the interest rate expected to remain unchanged at its current 6.5%. The Fed held the benchmark interest rate in the current 3.50%-3.75% range for the fourth consecutive time this year, at Kevin Warsh's first meeting as head of the Fed. The unanimous decision, in line with expectations, was based on a scenario of expanding economic activity, despite uncertainty surrounding the conflict in the Middle East, with the labor market mirroring this trend. However, inflationary pressures persist and remain above the medium-term target of 2.0%, tipping the scales in favor of maintaining a restrictive stance.

Weekly Monitor

International

This week's focus in the United States will be on the release of the PCE inflation figure for May—the Fed's preferred measure of inflation for monetary policy decisions. Expectations are for a 4.1% annualized increase and a 3.4% increase in core inflation. The final estimate of first-quarter GDP will also be released, projecting annualized growth of 1.6%. Additionally, preliminary June Purchasing Managers' Indices (PMIs)—leading indicators of economic activity—will be published for the United States and the Eurozone. Finally, in Latin America, Mexico will hold another monetary policy meeting, with the interest rate expected to remain unchanged at its current 6.5%.

The Fed held the benchmark interest rate in the current 3.50%-3.75% range for the fourth consecutive meeting this year, at Kevin Warsh's first meeting as Fed Chair. The unanimous decision, in line with expectations, was based on a scenario of expanding economic activity, despite uncertainty surrounding the conflict in the Middle East, with the labor market mirroring this trend. However, inflationary pressures remain persistent, exceeding the medium-term target of 2.0%, which has tipped the scales in favor of maintaining a restrictive stance.

In its quarterly update of macroeconomic projections, the economic growth forecast for 2026 was slightly revised downward to +2.2%, and the unemployment forecast to 4.3%. In contrast, the inflation estimate was raised: headline inflation is now expected to reach +3.6% year-on-year, compared to the previous +2.7%, while core inflation (excluding food and energy) is projected at +3.3% versus +2.7% in March. In terms of monetary policy, a reversal in the short-term stance is observed, resulting in a higher interest rate environment. The expectation for 2026 is that rates will remain unchanged or rise by the end of the year.

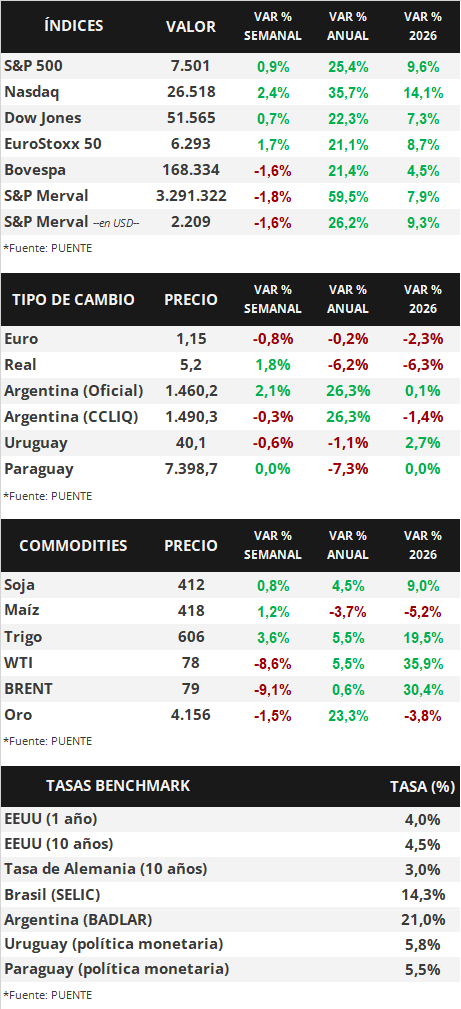

In this environment, US Treasury yields traded mixed across the curve during the week. While the 1-year Treasury yield widened from 3.84% to 3.97% and the 3-year yield from 4.14% to 4.19%, the 10-year yield compressed from 4.48% to 4.45%. Meanwhile, investment-grade corporate bonds (LQD ETFs) finished with a yield of 5.6%. For their part, the main US stock indices extended their upward trend, with the Nasdaq leading the way with a weekly gain of 2.4%.

On Sunday, delegations from the United States and Iran met in Switzerland and agreed to establish a committee to advance negotiations toward a peace agreement within the next 60 days.

In the Eurozone, final inflation for May was +0.1% month-on-month and +3.2% year-on-year, while core inflation was +0.2% month-on-month and +2.6% year-on-year, slightly above the expected +2.5%. It is worth noting that year-on-year figures showed an acceleration compared to April, remaining above the European Central Bank's target. Against this backdrop, the euro fell 0.8% to $1.15 per euro.

Meanwhile, the Bank of England also left its benchmark interest rate unchanged at 3.75%. In contrast, the Bank of Japan raised its policy rate by a quarter of a percentage point to 1.0%, the highest level in three decades. Both decisions were in line with projections, reflecting concerns about increased inflationary pressures.

In Latin America, the Central Bank of Brazil bucked the global trend by cutting its benchmark interest rate again to 14.25% from the previous 14.5%, as expected. Finally, in Chile, the cost of financing remained unchanged at 4.5% annually. As a result, the real strengthened by 1.8% to 5.15 reais per dollar, and the Chilean peso gained 0.7% week-on-week.