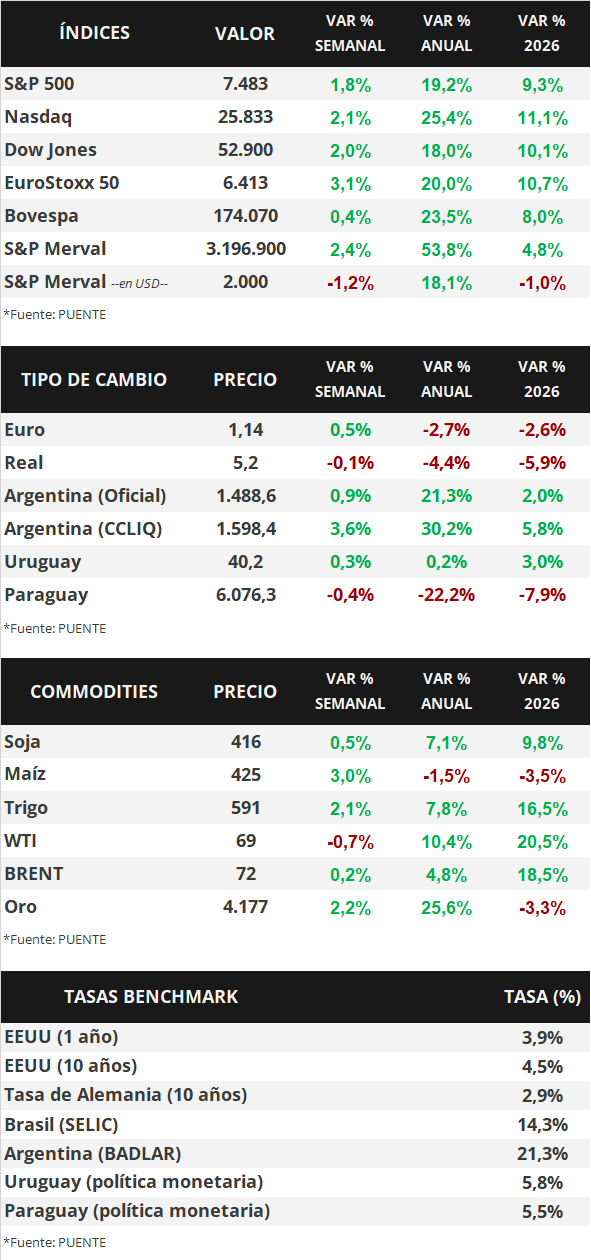

In the United States, 57,000 new jobs were created in June, fewer than the 113,000 projected by analysts and the revised figure for May (129,000 jobs). However, the unemployment rate remained at 4.2%, below expectations. Against this backdrop, US Treasury yields widened during the week, primarily in the medium and long ends of the curve, with the 1-year bond yield reaching 3.92% and the 10-year bond yield 4.48%. Meanwhile, major stock indices closed higher, with the Dow Jones reaching a new all-time high. This week, attention will focus on the release of the minutes from the Federal Reserve's (Fed) latest monetary policy meeting, in which the Fed decided to keep the benchmark interest rate unchanged at 3.75%. In a scenario of higher short-term inflationary risks and a stable labor market, the benchmark interest rate is expected to remain at historically high levels, allowing for higher nominal returns for longer periods for investment-grade bonds, with the 5-year maturity segments of the curve looking attractive.

Weekly Monitor

International

This week's focus in the United States will be on the release of the minutes from the Fed's latest meeting, in which the benchmark interest rate remained unchanged at 3.75% and was expected to remain elevated for longer. Also expected to be released are the retail sales figures—a proxy for economic activity—and the trade balance for May. Meanwhile, in the Eurozone, data on retail sales and wholesale prices for May will be published. Finally, in Latin America, June inflation figures will be released for Brazil, Mexico, and Chile, with the latest figures showing year-on-year increases of 4.7% for Brazil and 3.9% for Mexico and Chile, respectively.

In the United States, 57,000 new jobs were created in June, representing the most modest performance in the last four months. This result fell well short of the 113,000 jobs estimated by analysts and the revised figure of 129,000 for May (down from 172,000). Meanwhile, the unemployment rate fell slightly to 4.2%, compared to the expected 4.3%.

In this environment, US Treasury yields widened during the week, primarily in the medium and long ends of the curve. The 1-year Treasury yield rose from 3.91% to 3.92%, the 3-year yield from 4.09% to 4.16%, and the 10-year yield from 4.37% to 4.48%. Investment-grade bonds (LQD ETFs) finished with a yield of 5.6%. For their part, the main US stock indices showed widespread gains, with the Dow Jones reaching a new all-time high.

In the Eurozone, preliminary inflation for June slowed compared to May, falling short of expectations across the board. Specifically, it registered -0.1% month-on-month and +2.8% year-on-year, versus the 3.0% forecast, while the core inflation rate (excluding food and energy) rose 0.2% month-on-month and 2.4% year-on-year, compared to a projected 2.5%. Against this backdrop, the euro closed at $1.14 after rising 0.5% for the week, and the yield on the 10-year German Treasury bond closed at 2.94%.

Regarding the performance of Latin American sovereign debt, the yields on 10-year dollar-denominated bonds in Brazil and Mexico fell from 6.08% and 6.00% at the beginning of the previous week to their current levels of 6.03% and 5.93%, respectively.