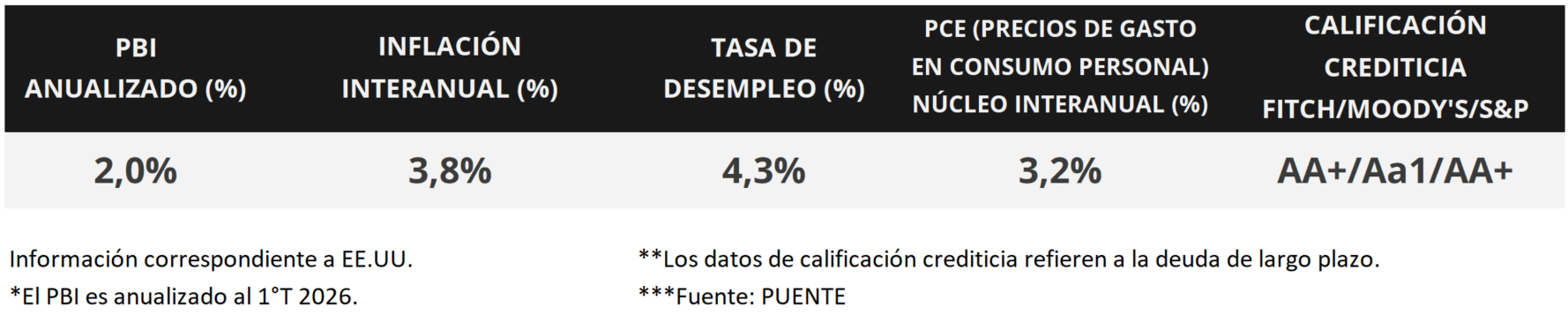

In the United States, the first-quarter earnings season is winding down, with 94% of companies reporting their results, collectively showing a 28.4% year-over-year increase in earnings per share. This performance is driven by the "Magnificent Seven," whose earnings have risen 63.2% year-over-year for the period. Against this backdrop, US Treasury yields traded mixed, with the 1-year bond at 3.84% and the 10-year bond at 4.56%, while the Dow Jones stock index reached a new all-time high for the week. This week's focus will be on the release of the April Personal Consumption Expenditures (PCE) price index—the Federal Reserve's preferred inflation measure for monetary policy decisions—with projections of a 3.9% year-over-year increase and a 3.3% increase for the core (food and energy) component. The second of three estimates for Gross Domestic Product (GDP) for the first quarter will also be released, with an expected annualized growth rate of 2.1%. With the Fed observing increased inflationary pressures in the short term, the outlook is that the benchmark interest rate (currently at 3.75%) will remain historically high. This allows for higher nominal returns now compared to what could be obtained later on for investment-grade bonds, making the up to five-year maturities on the yield curve particularly attractive.

Weekly Monitor

International

This week's focus in the United States will be on the release of the PCE inflation figure—the Fed's preferred indicator for monetary policy decisions—for April, with an estimated year-over-year increase of 3.9% and a core inflation rate of 3.3%. The second estimate of Q1 GDP will also be released, with expectations of annualized growth of 2.1%. In Latin America, the spotlight will be on Brazil's Q1 GDP, with the latest figure showing a 1.8% year-over-year increase.

With Q1 earnings season nearing its end, Nvidia—the last of the "Magnificent Seven" companies to report—has released its results, reporting earnings per share and revenue above expectations. It's worth noting that of the 94% of S&P 500 companies that have already reported, 84% exceeded earnings estimates and 81% exceeded revenue estimates. Meanwhile, the "Magnificent Seven" companies saw earnings rise by 63.2% year-over-year, while the remaining 493 companies experienced a 17.4% increase. Overall, earnings grew by 28.4% year-over-year.

The minutes from the Fed's latest monetary policy meeting reveal the concerns of the Federal Open Market Committee (FOMC) members, which led to strong dissent regarding keeping the benchmark interest rate unchanged in April. However, most of them agreed that if inflation continues to climb and rises above the 2.0% medium-term target, a slightly more restrictive stance would be advisable.

On the other hand, preliminary data for May on the sectoral Purchasing Managers' Indices (PMIs) in the United States exceeded 50 points in all cases, the threshold that separates expansion from contraction in economic activity. While the manufacturing index stood at 55.3 points, the services index reached 50.9 points.

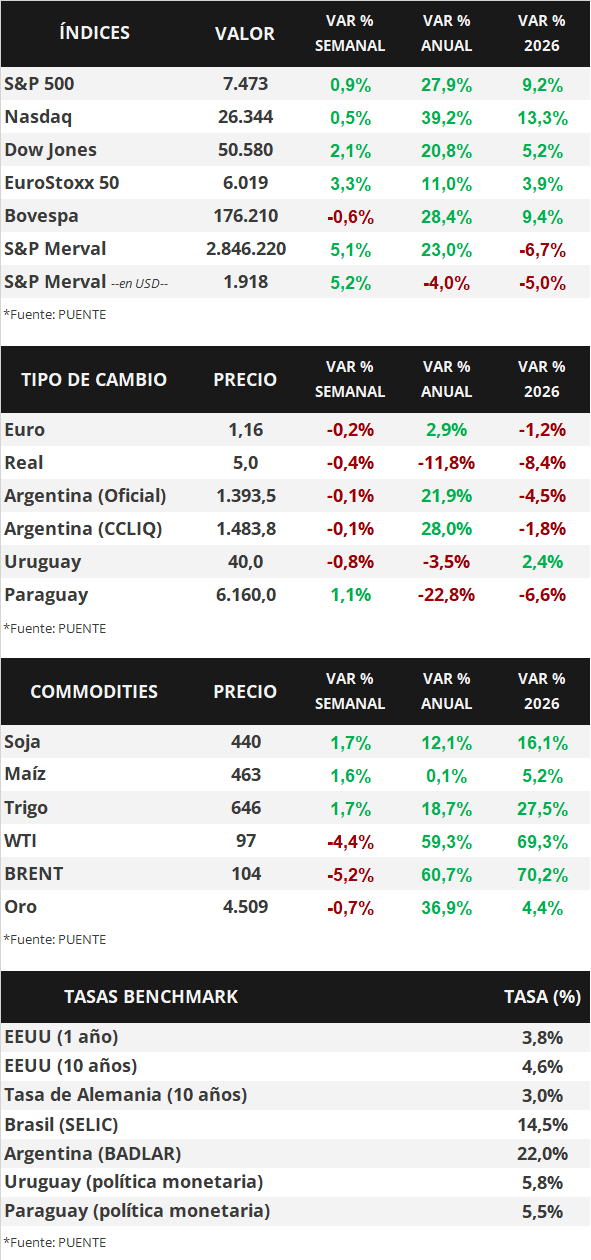

In this environment, US Treasury yields showed mixed performance this week. The 1-year Treasury yield increased from 3.81% to 3.84%, the 3-year yield rose from 4.14% to 4.17%, while the 10-year yield fell from 4.60% to 4.56%. Meanwhile, investment-grade bonds (LQD ETFs) finished with a yield of 5.6%. For their part, the main US stock indices closed higher, with the Dow Jones reaching a new all-time high.

In the Eurozone, April inflation was in line with estimates, registering 1.0% month-on-month and 3.0% year-on-year, while core inflation rose 0.9% month-on-month and 2.2% year-on-year. Meanwhile, the May sectoral PMIs were lower than expected across the board, with manufacturing registering 51.4 points and services 46.4 points.

In Latin America, first-quarter GDP figures were released for Chile and Mexico. In Chile, GDP contracted 0.5% year-on-year, compared to the projected 0.1% growth. In Mexico, GDP grew 0.2% year-on-year, slowing compared to the previous quarter, but slightly exceeding expectations.