Morning View

U.S. stock indices rebounded sharply yesterday

International

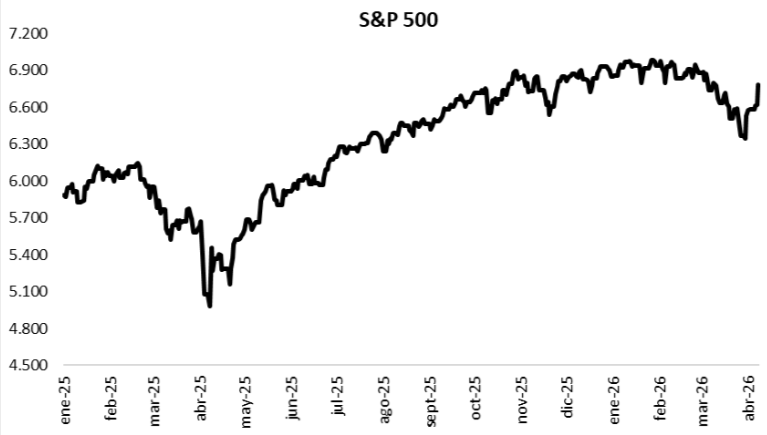

Yesterday, the major U.S. stock indices rebounded sharply following news that the United States and Iran had agreed to a two-week ceasefire while negotiating the terms of a more lasting peace. The S&P 500 rose +2.5%, while the Nasdaq and the Dow each rose +2.8%. As a result, year-to-date, they have accumulated changes of -0.9%, -2.6%, and -0.3%, respectively. The effect was largely global, with the European EuroStoxx 50 index also rising +5.0%, while Japan’s Nikkei gained +5.4%.

Meanwhile, the U.S. Treasury yield curve saw few changes. The yield on the 1-year Treasury note rose slightly from 3.63% to 3.67%, while the 3-year Treasury note remained at 3.81%. For the 10-year Treasury note, the yield also remained unchanged at 4.29%.

Commodities saw mixed trading during the session, led by movements in oil. WTI crude closed at $96.70, down 14.4%, while Brent closed at $96.40, down 11.8%. Meanwhile, gold rose slightly by +0.3% and closed at $4,719.50 per ounce, while soybeans also rose +0.3% and closed at $426.80 per ton.

Despite initial announcements, U.S. President Donald Trump stated that U.S. military forces remain on combat alert and will resume operations if negotiations fail. The truce shows signs of fragility because shipping in the Strait of Hormuz remains minimal, and because Israel has intensified its military campaign in Lebanon, claiming that this front is not part of the agreement reached with Iran.

Source: PUENTE Hnos, Bloomberg

The United States and Iran agree to a two-week ceasefire

International

Yesterday, after the market closed, news broke that the United States and Iran had agreed to a two-week ceasefire, contingent on Iran’s commitment to reopen the Strait of Hormuz. The agreement, brokered by Pakistan, could pave the way for peace negotiations based on an Iranian proposal outlining 10 points to be addressed. Oil prices, for both WTI and Brent, have fallen by about 15% since the news broke.

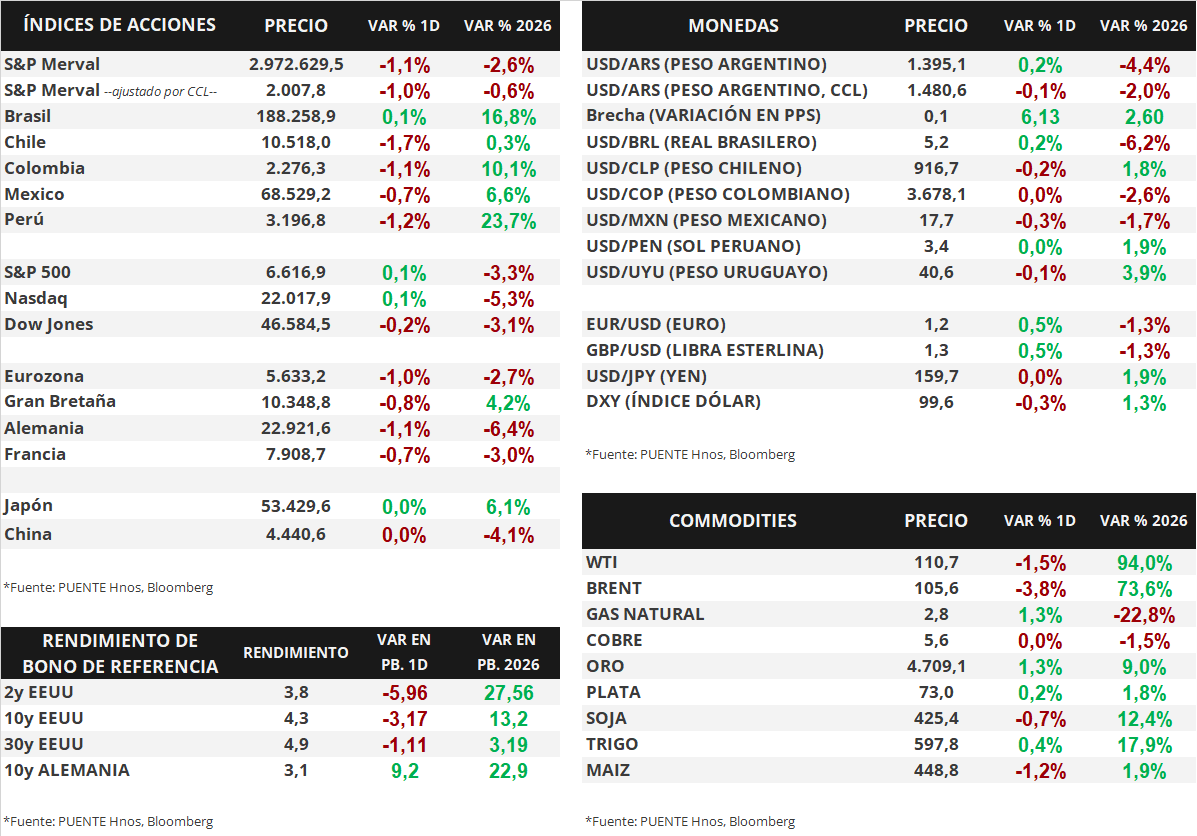

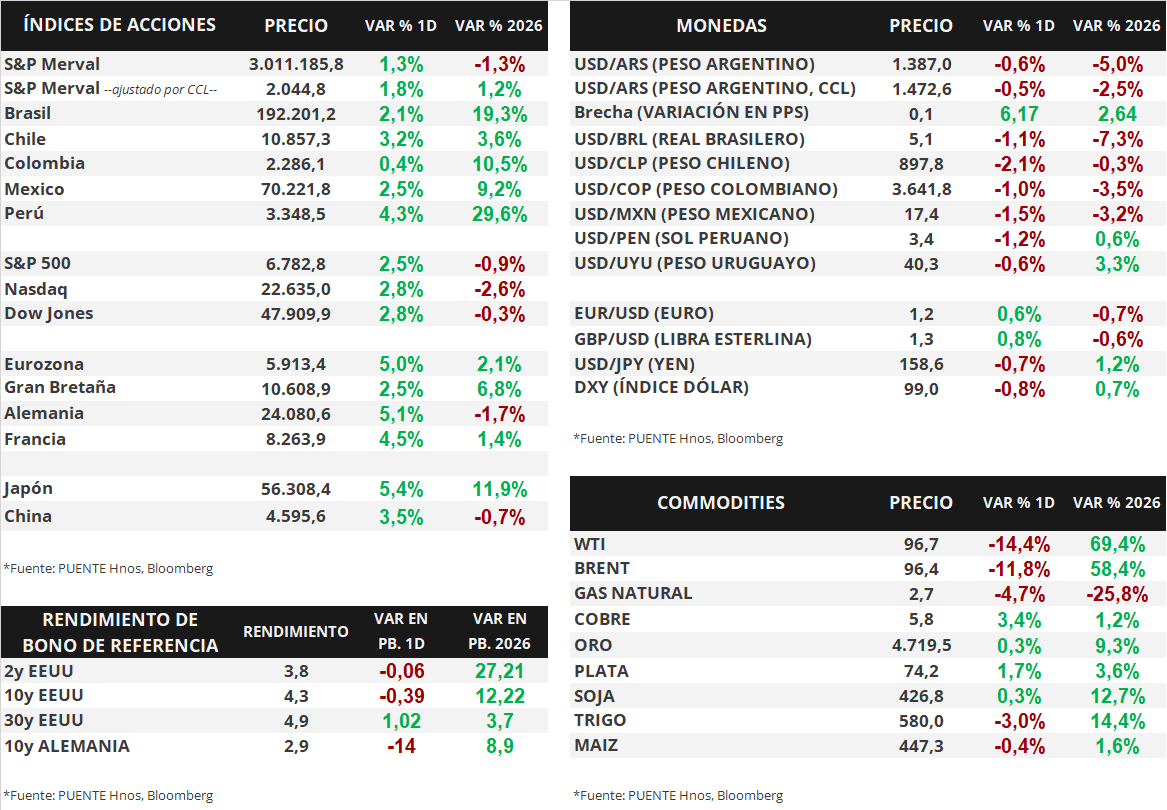

Major U.S. stock indices closed mixed on Tuesday, though they are advancing strongly in today’s pre-market trading. The S&P 500 closed up 0.1%, as did the Nasdaq, while the Dow Jones fell 0.2%. Thus, so far in 2026, the indices have accumulated changes of -3.3%, -5.3%, and -3.1%, respectively.

Meanwhile, the U.S. Treasury yield curve flattened yesterday. The yield on the 1-year bond fell from 3.69% to 3.63%, while the 3-year bond yield fell from 3.87% to 3.82%. For the 10-year bond, the yield fell from 4.33% to 4.30%.

Source: PUENTE Hnos, Bloomberg