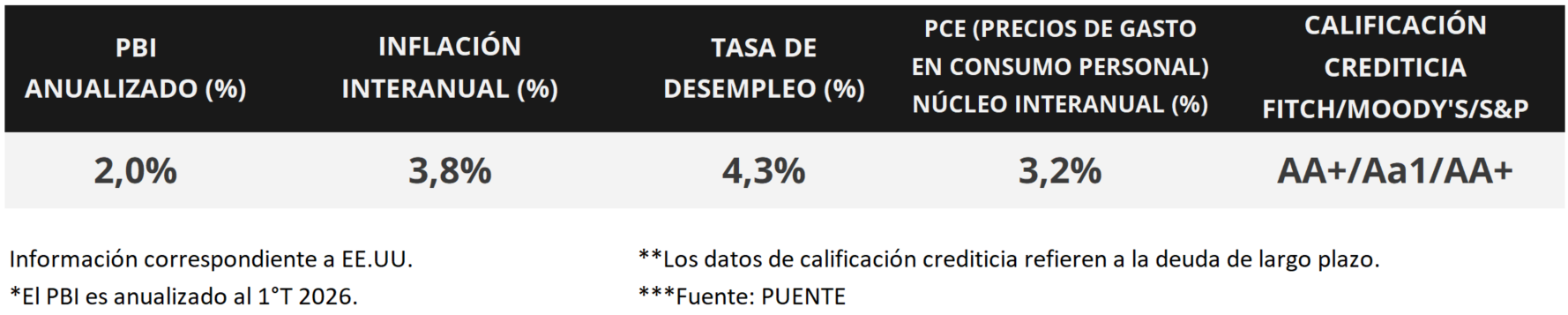

In the United States, April retail inflation accelerated to 3.8% year-on-year, the highest performance since May 2023 and exceeding the projected 3.7%, while core inflation (excluding food and energy) reached 2.8% year-on-year. Meanwhile, April wholesale inflation climbed to 6.0% year-on-year and core inflation to 5.2%, also above expectations. Against this backdrop, US Treasury yields saw significant increases, with the 10-year Treasury yield reaching 4.60%; while stock indices traded mixed, with the S&P 500 and Nasdaq hitting new all-time highs. This week's focus will be on Nvidia's Q1 earnings report, the last of the "Magnificent Seven" to release its financial results. The minutes from the Federal Reserve's (Fed) latest monetary policy meeting will also be released, revealing that the benchmark interest rate remained unchanged at 3.75%. Given the rising short-term inflationary risks, the expectation is that interest rates will remain at historically high levels, allowing for higher nominal returns now compared to those that could be obtained later on for investment-grade bonds. Therefore, it is advisable to position investors in maturities up to five years.

Weekly Monitor

International

This week's focus in the United States will be on the first-quarter earnings season, as Nvidia, the last of the "Magnificent Seven" to report its results, will be released. Meanwhile, the minutes from the Fed's latest monetary policy meeting will be published, along with preliminary sectoral Purchasing Managers' Indices (PMIs) for May in the United States and the Eurozone. In the Eurozone, final inflation figures for April will be released, projected to show a year-on-year increase of 3.0% and core inflation of 2.2%. In Latin America, the first-quarter GDP figures for Chile and Mexico will be published.

In the United States, the Consumer Price Index (CPI) rose 0.6% month-on-month and 3.8% year-on-year in April, slightly above the 3.7% projected by analysts and marking the strongest performance since May 2023. Meanwhile, core inflation advanced 0.4% compared to March and 2.8% year-on-year, also exceeding the expected 2.7%.

Wholesale inflation in April was higher than expected across the board, accelerating to 1.4% month-on-month and 6.0% year-on-year, while core inflation rose 1.0% month-on-month and 5.2% year-on-year. It is worth noting that the year-on-year figures are the highest since early 2023, due to the impact of the conflict in the Middle East.

Regarding the first-quarter earnings season, 91% of S&P 500 companies released their financial results. Of these, 84% exceeded earnings estimates and 80% exceeded revenue estimates. Overall, earnings grew by 27.7% year-over-year and revenue by 11.4%, surpassing analysts' consensus expectations.

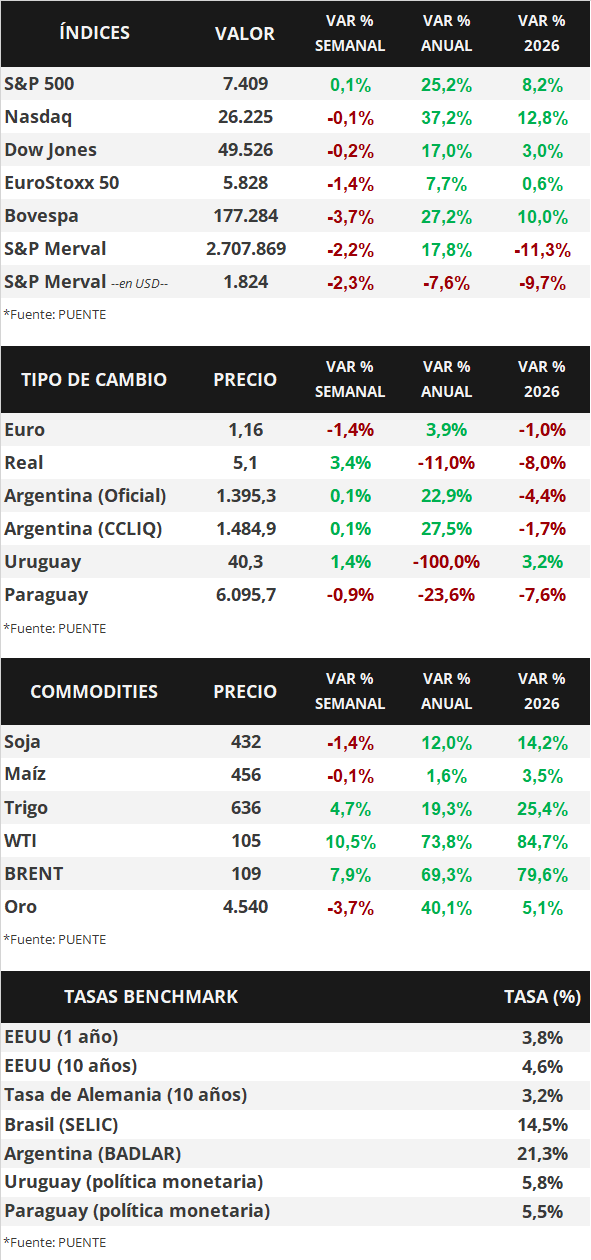

In this environment, US Treasury yields saw significant increases this week, primarily in the medium and long ends of the curve. The 1-year Treasury yield rose from 3.73% to 3.81%, the 3-year yield from 3.91% to 4.14%, and the 10-year yield from 4.36% to 4.60%. Meanwhile, investment-grade bonds (LQD ETFs) finished with a yield of 5.6%. For their part, the main US stock indices closed mixed, with the Nasdaq and the S&P 500 reaching new all-time highs.

In Latin America, Brazil's April inflation figures were released, coming in line with expectations at +0.7% month-on-month and +4.4% year-on-year, the latter figure marking the second consecutive month of increases. Against this backdrop, the real strengthened by 3.4% to 5.1 reais per dollar.