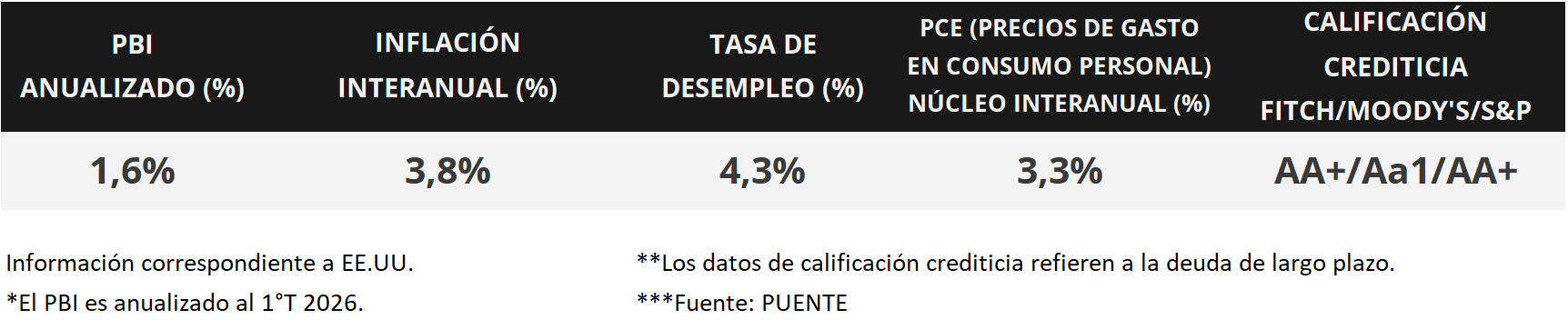

In the United States, the personal consumption expenditures (PCE) price index—the Federal Reserve's (Fed) preferred indicator for monetary policy decisions—accelerated slightly in April, registering a 3.8% annualized increase, the highest level since May 2013, and a 3.3% increase in the core PCE index, which excludes food and energy. In terms of economic activity, first-quarter GDP growth was revised downward, with annualized growth of 1.6% compared to the previously projected 2.0%. Against this backdrop, US Treasury yields compressed across the curve, with the 1-year Treasury yield at 3.77% and the 10-year Treasury yield at 4.44%, while stock indices reached new all-time highs at the end of the week. The focus this week will be on the release of data regarding the evolution of the labor market in May, with projections indicating the creation of 93,000 new jobs and a stable unemployment rate of 4.3%. With the expectation of persistently high inflation above the Fed's target of 2.0% annually, the benchmark interest rate (currently at 3.75%) is expected to remain historically high. This translates into higher nominal yields today compared to those that could be obtained later for investment-grade bonds, making it advisable to position oneself in the lower end of the yield curve with maturities up to 5 years.

Weekly Monitor

International

This week's focus in the United States will be on the May labor market data, with an estimated 93,000 jobs created and an unemployment rate of 4.3%. Meanwhile, developments are expected on the geopolitical front, amid anticipation of an agreement between the United States and Iran. Finally, the Eurozone will release preliminary May inflation figures, projecting an annual increase of 3.3% and a 2.4% increase in core inflation. The final estimate of first-quarter GDP will also be released, with projected annual growth of 0.8%.

In the United States, PCE inflation—the Fed's preferred inflation measure for interest rate decisions—rose 0.4% month-on-month and 3.8% year-on-year in April, the highest level since May 2023. Core inflation also advanced 0.2% month-on-month and 3.3% year-on-year. It is important to note that year-over-year growth accelerated during the month, although it was in line with expectations.

Meanwhile, first-quarter GDP grew at an annualized rate of 1.6%, according to the second of three estimates. This performance represents a downward revision compared to the previously projected 2.0% growth expected by the consensus of analysts.

In this environment, US Treasury yields experienced widespread compression across the curve during the week. The 1-year Treasury yield fell from 3.84% to 3.77%, the 3-year yield from 4.17% to 4.05%, and the 10-year yield from 4.56% to 4.44%. Meanwhile, investment-grade bonds (LQD ETFs) finished with a yield of 5.5%. For their part, the main US stock indices traded higher, reaching new all-time highs in all cases.

In Latin America, Brazil's Q1 GDP grew by 1.8% year-on-year, in line with analysts' consensus estimates and the same as the previous quarter, while the quarter-on-quarter figure was 1.1%, compared to the expected 1.0%. However, the Bovespa stock index closed down 1.4% for the week.