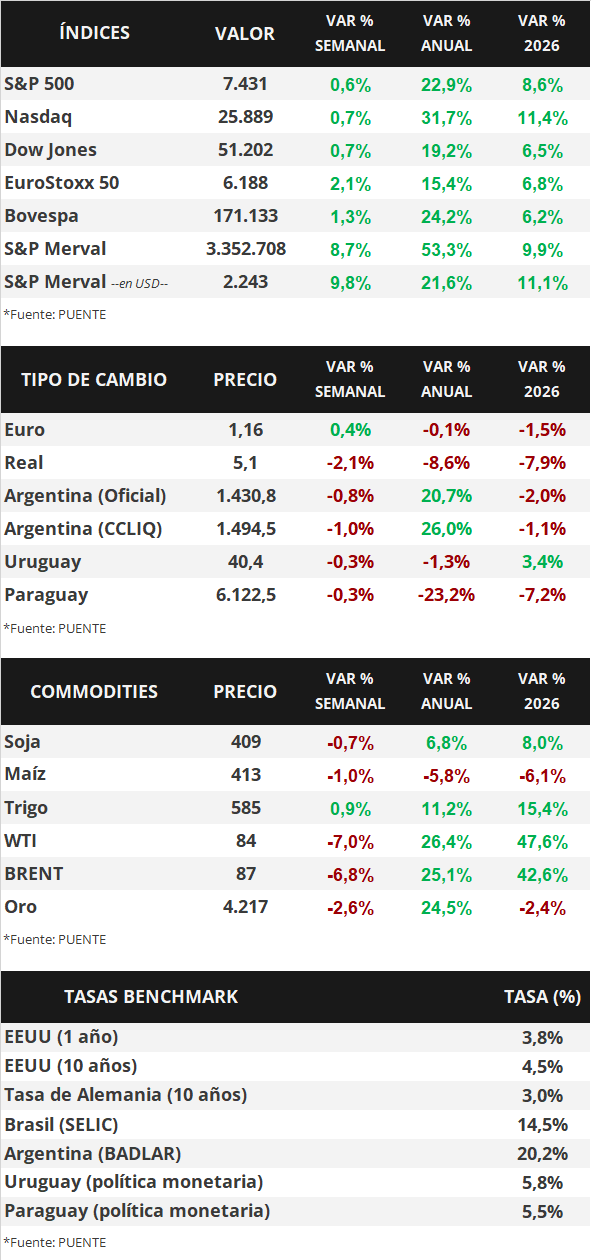

In the United States, the Consumer Price Index for May was in line with expectations in most cases, rising 4.2% year-over-year, the highest level in the last two years, and 2.9% in the core inflation measure (excluding food and fuel). Wholesale inflation also registered 6.5% year-over-year in May, the highest figure since November 2022, and 4.9% in core inflation. Against this backdrop, the US Treasury yield curve showed compression across all maturities, with the 1-year bond yield at 3.84% and the 10-year bond yield at 4.48%; while stock indices ended the week with slight gains. On the geopolitical front, over the weekend, Trump and the Pakistani Prime Minister announced the scope of a peace agreement between the United States and Iran, which will be signed in the coming days, bringing an end to the conflict in the Middle East. This week will be crucial, as the Federal Reserve (Fed) will make its first monetary policy decision under Chairman Warsh, with the expectation that the benchmark interest rate will remain unchanged at its current 3.75%. The quarterly update of macroeconomic outlook and interest rate path will also be released, providing further clues about the Fed's short-term monetary policy stance. Given this outlook of rising inflation exceeding the Fed's target of 2.0%, coupled with a stable labor market, it is expected that the cost of financing will remain historically high. This allows for higher nominal returns today compared to those that could be obtained later on for investment-grade bonds, making it appropriate to position oneself in the lower end of the yield curve, up to five years in maturity.

Weekly Monitor

International

This week's focus in the United States will be on the Fed's monetary policy meeting, Kevin Warsh's first as chairman, with expectations that the benchmark interest rate will remain in its current range of 3.5%-3.75%. The quarterly update on macroeconomic prospects and the interest rate path will also be presented, providing further insight into the direction of short-term monetary policy. Meanwhile, the signing of the agreement announced between the United States and Iran is expected next Friday in Switzerland, which would end the war in the Middle East. In the Eurozone, final inflation figures for May will be released, with year-on-year inflation estimated at 3.2% and core inflation at 2.5%. Finally, there will also be benchmark interest rate decisions in other countries: in the United Kingdom and Chile, rates are projected to remain unchanged at their current levels of 3.75% and 4.5%, respectively; in Japan, an increase to 1.0% from the current 0.75% is expected, while in Brazil, a quarter-point cut to 14.25% is anticipated.

In the United States, May inflation was in line with analysts' consensus expectations in most cases. Specifically, it registered a monthly increase of +0.5%, slightly lower than the previous figure, and +4.2% year-on-year, the highest performance in the last two years. Meanwhile, core inflation rose +0.2% monthly versus the expected +0.3%, and +2.9% year-on-year.

On the other hand, wholesale inflation in May came in above expectations, rising 1.1% month-on-month and 6.5% year-on-year, the latter representing the highest figure since November 2022. Meanwhile, core inflation showed a slight slowdown compared to April, registering 0.4% month-on-month and 4.9% year-on-year, both figures lower than anticipated.

In this environment, US Treasury yields compressed across most maturities during the week. The 1-year bond remained at 3.84%, the 3-year bond fell from 4.20% to 4.14%, and the 10-year bond dropped from 4.53% to 4.48%. Investment-grade bonds (LQD ETFs) finished with a yield of 5.5%. For their part, the main US stock indices closed with widespread gains, averaging 0.7% for the week.

The European Central Bank (ECB) raised its monetary policy rate to 2.4% from the previous 2.15%, in line with analysts' consensus expectations and after a year of keeping it unchanged. The committee justified the decision based on the sustained increase in the price level, which remains above the institution's medium-term target (2.0%) due to the impact of the conflict in the Middle East on energy prices. In this context, the euro rose 0.4% to $1.16 per euro, while the yield on the 10-day German Treasury bond closed at 3.0%.

In Latin America, May inflation figures were released for Brazil, Mexico, and Chile. While Brazil's inflation increased by 4.7% year-on-year, exceeding expectations and accelerating compared to the previous month, Mexico and Chile each registered a 3.9% year-on-year increase, lower than both expectations and April's figures. Consequently, exchange rates ended the week with declines of -2.1%, -1.4% and -1.7%, respectively.