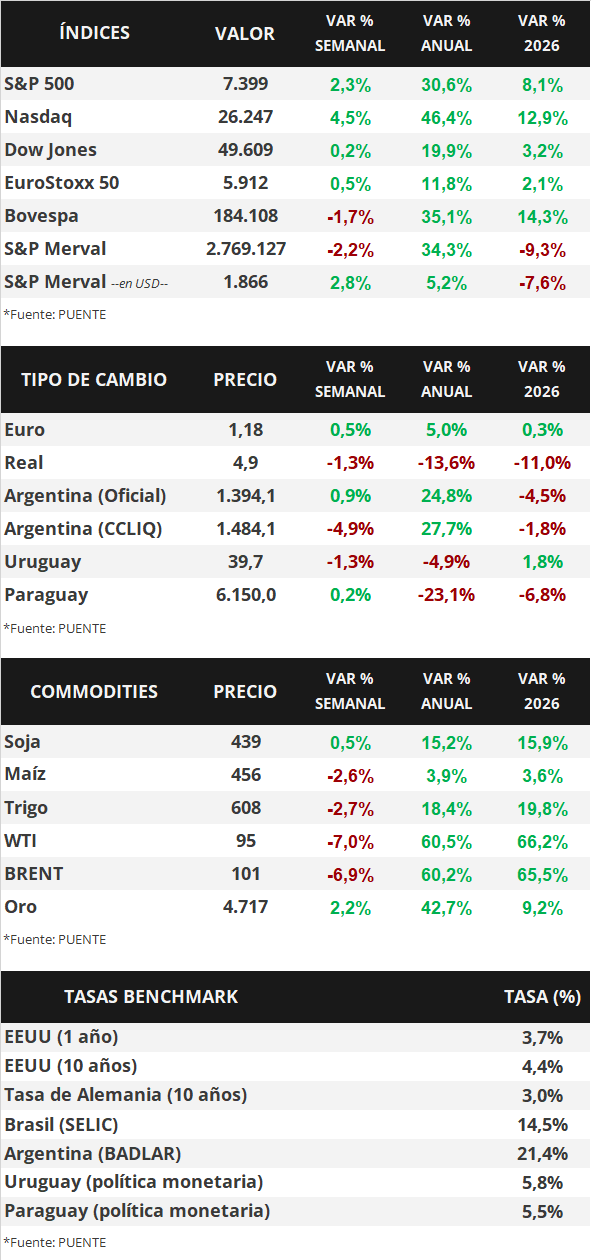

In the United States, the labor market's performance in April was a positive surprise, with 115,000 new jobs created, exceeding the 65,000 expected by analysts. The unemployment rate remained stable at 4.3% for the second consecutive month. Against this backdrop, stock indices continued their upward trend, with the S&P 500 and Nasdaq reaching new all-time highs. Meanwhile, US Treasury yields were mixed, with the 1-year Treasury yield at 3.73% and the 10-year yield at 4.36%. This week, April's retail inflation figures will be released, projected to show a year-over-year increase of 3.7%, and a 2.7% increase for the core inflation rate (excluding food and energy). The wholesale price index for the same month will also be published, as the first-quarter earnings season continues. With higher inflationary risks in the short term, the interest rate (currently at 3.75%) is expected to remain historically high, resulting in higher nominal returns at present compared to those that could be obtained later for investment-grade bonds, making it advisable to position oneself in tranches up to 5 years in duration.

Weekly Monitor

International

This week's focus in the United States will be on the release of the April Consumer Price Index (CPI), which is expected to show a year-over-year increase of 3.7%, with core inflation rising 2.7%. Additionally, wholesale inflation and retail sales figures—a proxy for economic activity—for April will be released. Meanwhile, the first-quarter corporate earnings season is underway, while developments regarding the conflict in the Middle East are awaited. In the Eurozone, March industrial production figures will be published, along with the second estimate of first-quarter GDP, which is expected to show annual growth of 0.8%. Finally, in Latin America, Brazil's April inflation figures will be released, with the latest reading showing a year-over-year increase of 4.1%.

In the United States, 115,000 new jobs were created in April, exceeding the consensus analyst expectation of 65,000, but falling short of the revised figure of 185,000 for March. Meanwhile, the unemployment rate remained stable at 4.3%.

Regarding the first-quarter earnings season, 89% of S&P 500 companies have now released their financial results. Of these, 84% exceeded earnings estimates and 80% exceeded revenue estimates. Overall, earnings are up 27.7% year-over-year and revenue is up 11.3%, both above expectations. This week, McDonald's, Palantir, Pfizer, KKR & Co., Walt Disney, CVS Health, and Kraft Heinz reported earnings per share (EPS) and revenue above expectations. Mercado Libre, HSBC, and Airbnb, however, only exceeded revenue projections but not EPS. This week, Alibaba, Cisco, Allianz, and Siemens, among other major companies, will report their results.

Against this backdrop, the US Treasury yield curve saw only slight changes during the week. The 1-year bond yield fell from 3.71% to 3.73%, the 3-year yield from 3.89% to 3.91%, and the 10-year yield from 4.38% to 4.36%. Meanwhile, investment-grade corporate bonds (LQD ETFs) finished with a yield of 5.5%. Elsewhere, the main US stock indices continued their upward trend, with the Nasdaq and the S&P 500 reaching new all-time highs during the week.

In Latin America, inflation in Chile accelerated to 4.0% year-on-year in April, surpassing the March figure but falling short of the 4.2% projected by analysts. Meanwhile, Mexico's inflation reached 4.45% annually, lower than both the previous week's figure and the estimate. This data was released prior to the monetary policy decision by the Bank of Mexico, which lowered the benchmark interest rate to 6.5% from the previous 6.75%. In this context, the exchange rates of Chile and Mexico fell by 1.1% and 1.6%, respectively.